Value Stocks: U.S. Drag, International Boost?

Key Takeaways

- Outside the U.S., value stocks have outperformed their benchmark.

- This is in contrast to the U.S., where value investing has underperformed over various timeframes.

- Investors can consider incorporating the value factor in their international allocations.

Value stocks are living a double life—and if you’re looking only at the U.S., you might be missing the plot. While value strategies have struggled on U.S. turf, markets beyond American borders tell a very different story.

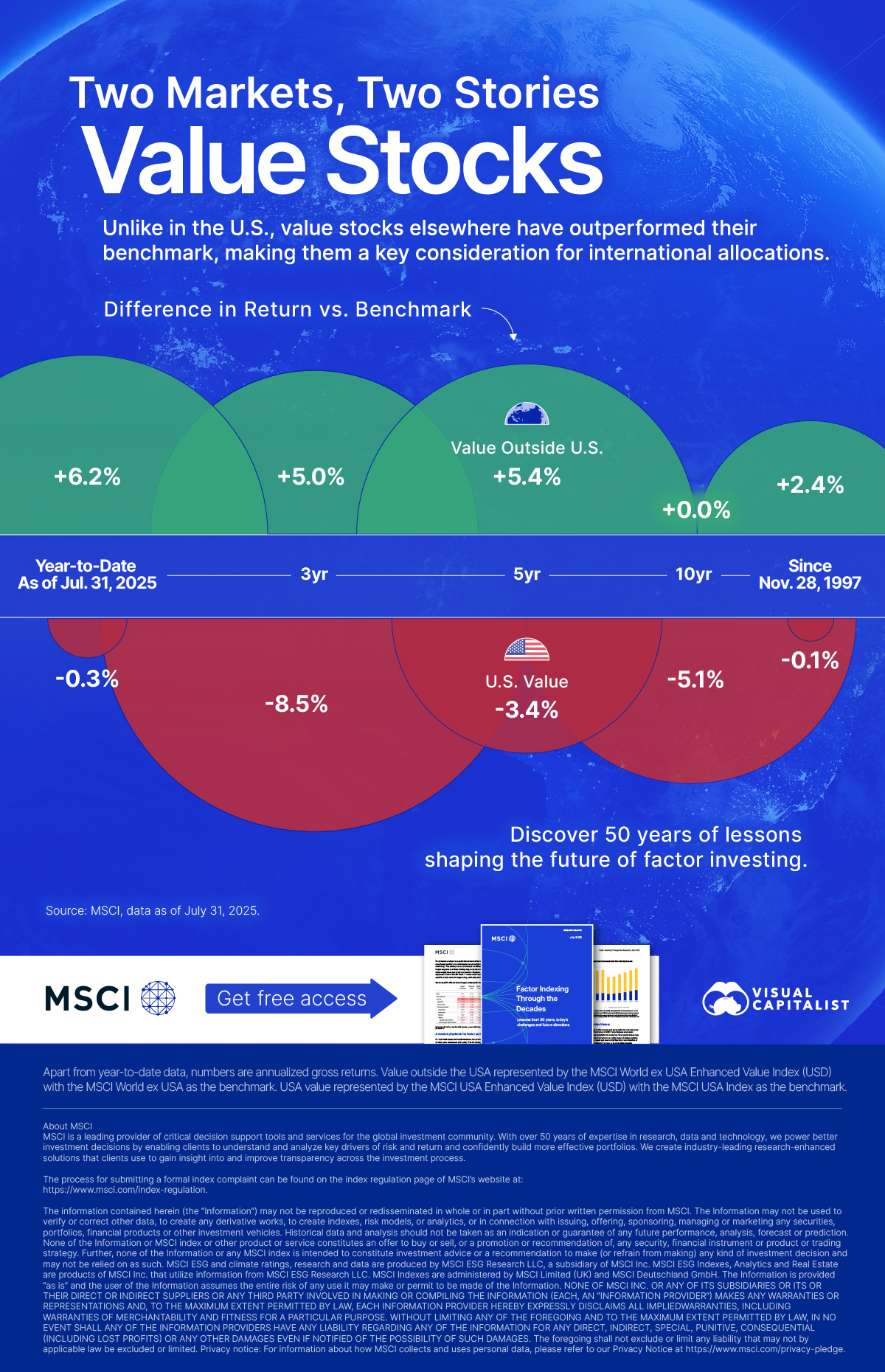

This graphic, in partnership with MSCI, shows how value stocks outside the U.S. have outperformed their benchmarks while underperforming domestically.

What is Value Investing?

Value investing involves buying stocks that appear undervalued. This means looking at metrics like price-to-book value, price-to-forward earnings, and enterprise value-to-cash flow from operations.

Value is one element of factor investing that investors can look at when targeting characteristics that can help explain the bulk of stocks’ risk and return.

The Performance of Value Stocks

In recent years, the success of the value factor looks very different depending on where the stocks are located. The table below shows the difference in return between the value index and its benchmark.

| Timeframe | Value Outside U.S. | U.S. Value |

|---|---|---|

| Year-to-Date | +6.2% | -0.3% |

| 3yr | +5.0% | -8.5% |

| 5yr | +5.4% | -3.4% |

| 10yr | +0.0% | -5.1% |

| Since Nov. 28, 1997 | +2.4% | -0.1% |

Source: MSCI, data as of July 31, 2025. Apart from year-to-date data, numbers are annualized gross returns. Value outside the U.S. represented by the MSCI World ex USA Enhanced Value Index (USD) with the MSCI World ex USA as the benchmark. U.S. value represented by the MSCI USA Enhanced Value Index (USD) with the MSCI USA Index as the benchmark.

Within the U.S., value stocks have lagged their benchmark over various timeframes. This was partly due to a long period of low interest rates and modest inflation which favors growth stocks. In particular, mega-growth stocks like the Magnificent Seven have dominated stock market performance in America. These stocks’ ultra-high valuations mean they are excluded by many value strategies.

However, in developed markets outside the U.S., value investing has seen stronger returns than its benchmark. Internationally, mega-cap stocks do not dominate the market, leaving more potential for value to outperform.

Financials, a core component of value strategies, saw a stronger rebound in markets like Europe, where banks were coming off years of negative rates. Unlike in the U.S., even modest post-COVID rate hikes significantly lifted margins. And with lower starting valuations in regions like Europe and Japan, these value-oriented banks had more room to rise as profitability improved.

A World of Value

While value stocks have underperformed in the U.S. and growth stocks have dominated the narrative, this is not the case elsewhere.

Historically, companies that appear undervalued have beaten their benchmarks in other developed markets. For the international allocations within portfolios, investors can consider incorporating value stocks.

Discover 50 years of lessons shaping the future in MSCI’s free report Factor Indexing Through the Decades.

-

Investor Education1 month ago

Investor Education1 month agoWhich Countries Are Winning the Resilience Race?

Discover which economies lead in climate resilience firms—and how investors can spot opportunities in this growing market.

-

Investor Education1 month ago

Investor Education1 month agoChina’s Economy vs. Market Cap: A Global Imbalance

China’s economy is a large percentage of global GDP, but the country has a small weight in equity markets—here’s what investors need to know.

-

Investor Education3 months ago

Investor Education3 months agoA New Framework for Personalized Financial Portfolio Alignment

The MSCI Similarity Score compares a client’s financial portfolio to a model portfolio based on risk exposures, allowing for personalization.

-

Green4 months ago

Green4 months agoTracking Emissions: Corporate Concentration and Climate Progress

Just 1% of companies are responsible for the majority of public company emissions. See the progress companies are making to reduce emissions.

-

Technology8 months ago

Technology8 months ago3 Reasons Millennials Are Driving the AI Revolution

Millennials are more likely to accept AI than older generations. What other factors could help them drive the AI revolution?

-

Technology10 months ago

Technology10 months agoThe Fintech Frontier: How Digital Wallets Are Changing Payments

Digital wallets have become the top payment method thanks to their convenience. How can investors track innovation in fintech companies?

-

Healthcare11 months ago

Healthcare11 months agoCharted: Deaths Related to Bacterial Infection vs. Research Efforts

Globally, nearly 14% of deaths are related to a bacterial infection—but research isn’t keeping up with the need for new treatments.

-

Healthcare11 months ago

Healthcare11 months agoVisualizing the Rise of Antibiotic Resistance

Antibiotic resistance has nearly tripled in the last two decades, meaning treatments may no longer work for some bacterial infections.

-

Technology1 year ago

Technology1 year agoCharting the Next Generation of Internet

In this graphic, Visual Capitalist has partnered with MSCI to explore the potential of satellite internet as the next generation of internet innovation.

-

Investor Education1 year ago

Investor Education1 year agoHow MSCI Builds Thematic Indexes: A Step-by-Step Guide

From developing an index objective to choosing relevant stocks, this graphic breaks down how MSCI builds thematic indexes using examples.

-

Markets2 years ago

Markets2 years agoWeathering Physical Climate Risks: A Guide for Financial Professionals

Physical hazards like fires pose climate risks for companies, due to the added costs of asset damage and business interruption.

-

Green2 years ago

Green2 years agoVisualized: What Are the Climate Risks in a Portfolio?

This infographic shows the effects of climate change on investments, and how climate risks may affect a portfolio’s value.

-

Green2 years ago

Green2 years agoVisualized: An Investor’s Carbon Footprint, by Sector

Which sectors are the largest contributors to emissions? From energy to tech, this graphic shows carbon emissions by sector in 2023.

-

Investor Education2 years ago

Investor Education2 years agoWhich Climate Metrics Suit Your Investment Goals Best?

When selecting climate metrics, it is important to consider your purpose, the applicability and acceptability of the climate strategy, and the availability of historical data.

-

Healthcare2 years ago

Healthcare2 years agoInnovation in Virology: Vaccines and Antivirals

Vaccine development has grown six-fold since 1995. Learn how virology, the study of viruses, is driving innovation in the healthcare industry.

-

Misc2 years ago

Misc2 years agoInfographic: Investment Opportunities in Biotech

Capture the investment opportunities in biotech with the MSCI Life Sciences Indexes, which target areas like virology and oncology.

-

Technology2 years ago

Technology2 years agoIndustrial Automation: Who Leads the Robot Race?

This graphic from MSCI shows the pace of industrial automation across leading countries like China and the U.S.

-

Technology2 years ago

Technology2 years agoRanking Industries by Their Potential for AI Automation

AI automation is expected to impact some industries more than others. See the latest projections in this infographic.

-

Markets2 years ago

Markets2 years agoHow Institutional Investors Can Approach Digital Assets

Digital assets are gaining popularity due to their return potential and decentralized nature. How can institutional investors get exposure?

-

Technology3 years ago

Technology3 years agoClassifying Digital Assets With a New Framework: Datonomy

How can investors get clarity on the thousands of digital assets available? A new structure classifies digital assets by their use cases.